As the third open enrollment period winds down on the health insurance marketplaces, one thing hasn’t changed much since the online exchanges opened: It’s still often hard to find out whether a plan covers abortion services.

The health law requires insurers to say one way or the other, and they have gotten better about reporting abortion coverage details this year, advocates on both sides agree. But the federal government has yet to put out final instructions on how insurers should handle the issue on their summary of benefits and coverage overview. Lacking specific instructions about what to say and where to say it, many insurers have simply left the information out of the summary, advocates said.

That leaves consumers in a bind. “It’s not easy to figure out whether a plan covers abortion and if it does, to what extent,” says Kinsey Hasstedt, a public policy associate at the Guttmacher Institute, a reproductive health research organization that supports abortion rights.

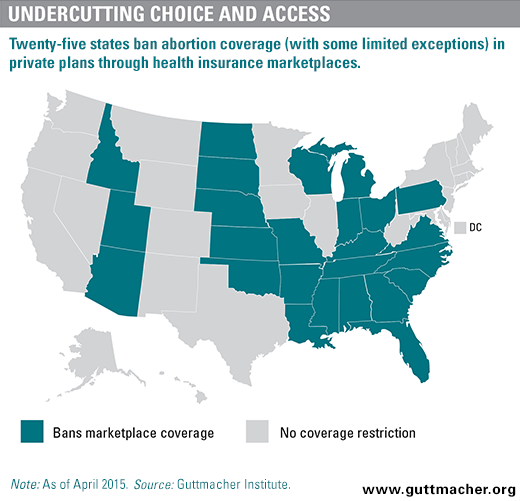

The health law lets states decide whether marketplace plans can cover abortion services. Half of states ban abortion coverage to some extent, often limiting it to cases of rape, incest or if the mother’s life is endangered, the standard the federal government uses for coverage in its employees’ plans and for health care programs, such as Medicaid.

However, even in states that permit insurers to cover abortion beyond the limited exceptions, marketplace plans may not have that benefit.

“In Texas, there’s no ban on abortion services, but depending on where you live, you may not have the option to choose a plan that includes abortion coverage,” said Alina Salganicoff, director of women’s health policy at the Kaiser Family Foundation (KHN is an editorially independent program of the foundation).

The lack of easily accessible information makes it hard to know whether the number of plans that currently provide abortion services on the exchanges is increasing or decreasing.

Advocates on both sides of the issue have their eyes on multi-state plans. To encourage competition, the health law called for at least two multi-state plans to be offered on every state marketplace by 2017, at least one of which excluded abortion services. In subsequent guidance, the Office of Personnel Management, which administers the multi-state program, said that multi-state insurers had to offer at least one silver and one gold level plan that excludes abortion coverage starting this year.

But the multi-state plan program is struggling. The number of states offering multi-state plans dropped to 32 plus the District of Columbia in 2016, down from 35 last year.

But the multi-state plan program is struggling. The number of states offering multi-state plans dropped to 32 plus the District of Columbia in 2016, down from 35 last year.

In those states, most multi-state plans don’t cover abortion, and the coverage information is easy to find, said Genevieve Plaster, a researcher at the Charlotte Lozier Institute, which opposes abortion. Of the 261 multi-state plans available in 2016, just four plans in two states — Connecticut and Alaska — provide abortion services, according to OPM.

However, abortion opponents said that because multi-state plans aren’t yet available in every state, there’s no guarantee consumers can find a plan that doesn’t cover abortion if that is their priority. In two states, Hawaii and Vermont, for example, all plans available cover abortion. Neither state has multi-state plans.

Abortion-rights supporters have a different beef with the multi-state plan program. They say it’s not fair to require the marketplace to offer plans that exclude abortion without also requiring plans that include abortion coverage. They also take issue with OPM’s decision that insurers must offer two multi-state plans that exclude abortion coverage, instead of the single one that the law requires.

OPM isn’t considering any changes to the program at this time, a spokesman said.

In the meantime, advocates on both sides hope that the final instructions for the coverage summaries will make it easier for consumers to learn whether plans cover abortion.

Questions remain about where in the eight-page summary of benefits and coverage the information appears: Some advocates want it near the section that describes covered services “if you are pregnant,” rather than under “excluded services and other covered services,” as the federal government has proposed.

And advocates on all sides agree that the language describing abortion services needs to be clear and consistent rather than the mishmash of descriptions that appear in current documents, where it may be called “interruption of pregnancy” or “elective termination of a normal pregnancy,” among other terms.

In a final regulation released last June, federal regulators said they would clarify requirements for the language and placement of abortion services in the coverage summary in the final template, which was scheduled to be finished this month.

“We’re still waiting for that,” said Gretchen Borchelt, vice president for health and reproductive rights at the National Women’s Law Center.

The Centers for Medicare and Medicaid Services didn’t respond to a request for information about when the new template would be released. The 2016 enrollment ends Jan. 31.

Please contact Kaiser Health News to send comments or ideas for future topics for the Insuring Your Health column.